A Dutch Lesson on Redefining Retirement Solutions

How are CIOs responding to the great DB to DC shift as the rest of Europe looks on?

3 ott 2024

What is Mario Draghi's recipe to reboot Europe?

In early September, Mario Draghi, the former Italian Prime Minister released a report that delivered a striking assessment of the European Union’s economic health and called for a multi-pronged approach to close its widening gap with its peers, notably the U.S. and China.

A slow “agony” of decline is what Europe should expect if it does not get its act together to improve economic growth, according to Draghi. The 400-page report is unusually direct in its analysis and highlights multiple areas where Europe is falling behind.1 It was commissioned by European Commission President Ursula von der Leyen.

They include areas ranging from the “tech transition” where Europe relies on other countries for over 80% of its digital products and services to gas prices which are three to five times compared to the U.S.

The policy blueprint on how the EU needs to change its approach has prompted analysts to draw parallels with Draghi’s “whatever it takes” speech in July 2012 during his term as the European Central Bank President, widely considered as the turning point of the sovereign debt crisis.

A key part of the agenda is about reducing regulatory burden.

For example, the report recognises that while securitization markets have thrived in the U.S., Japan, Australia and other jurisdictions post-global financial crisis, these markets are nowhere in Europe. While the regulatory and supervisory approaches on securitization are very similar across the globe, the footprint in Europe has been much heavier in its application than in other jurisdictions.

However, there seems to be political appetite to address this.

Other key recommendations in the report include rethinking EU competition rules for strategic industries, move towards regular issuance of debt to enable joint investment projects, improving decision-making processes and developing a foreign economic policy in which defence instruments and partnerships are used more strategically.

“A large focus of the Draghi report is to formulate an EU level industrial policy which is geared towards developing European industries for certain sectors compared to areas where there is no competitive advantage,” said Taggart Davis, Vice President, Government Affairs at EMEA.

“He is essentially saying, let’s figure out the industries where it makes sense to throw our collective industrial and financing firepower rather than try to boil the ocean.”

To achieve these objectives, the report calls for a minimum annual investment of 750-800 billion euros corresponding to around 5% of EU GDP, reversing a multi-decade decline across most large European economies.

This is unprecedented. For comparison, the additional investments provided by the Marshall Plan between 1948-51 to rebuild Europe amounted to around 1-2% of GDP annually.

However, Draghi’s recommendations venture into politically sensitive territory and have already come under political criticism.2 For example, his proposals for more regular issuance of joint European debt have already run into opposition from Germany and other Member States who have traditionally opposed greater risk sharing at EU level.

But the EU’s need to jump start its struggling economy is more urgent than ever before. The region is entering the first period in its recent history in which growth will not be supported by rising populations with the report estimating that by 2040, the workforce is projected to shrink by close to 2 million workers each year.

If the EU were to maintain its average productivity growth rate since 2015, it would only be enough to keep GDP constant until 2050 – at a time when the EU is facing a series of new investment needs that will have to be financed through higher growth.

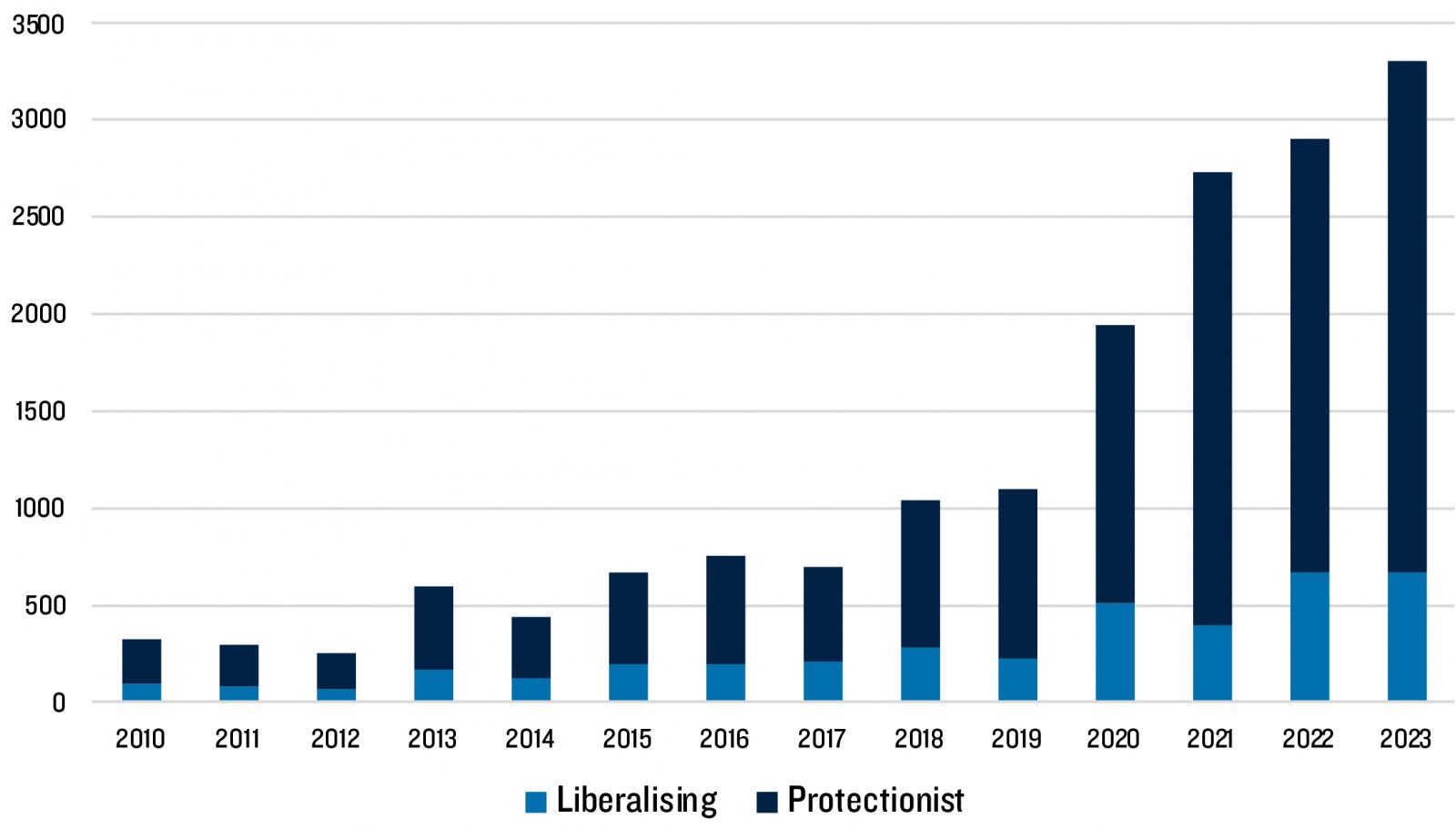

Source: Global Trade Alert, 2024

A recurring theme of the report is to develop a strong foreign economic policy. Through strategic partnerships such as competition policy, foreign direct investment screening, procurement markets and regulatory measures, Europe can leverage access to its market by non-EU companies in a way that helps secure its priorities and combats unfair trade practices.

This would be linked with an industrial policy under which the EU would seek to protect nascent future-oriented industries and IP through measures such as requirements for joint ventures, and screening of outbound investment.

This is in response to the broader observation by Draghi that the multilateral rules-based system which has served the global economy well for decades, is damaged, in decline, and increasingly less effective at protecting the EU from unfair competition with the region up against Chinese state-sponsored competition and the effects of the U.S. Inflation Reduction Act. As the report bluntly states: “The era of open global trade governed by multilateral institutions looks to be passing.”

“The name of the game is developing local markets and growth drivers even if that means shedding some of the globalist attitudes the EU had in the past, or at least supporting the multilateralist order, but ‘less naïvely’ than in the past,” said Davis. “It is like do we need investment restriction here or do we need a trade barrier there?”

Draghi’s report will be a huge positive for the EU if implemented. Fiscal spending will boost growth if it involves productive investments as markets will price that as a positive demand shock in the short term and a productive supply catalyst in the long term.

While the increased spending may potentially translate into higher interest rates as the central bank will likely lean against the positive demand impulse, risk markets will embrace the pro-growth features of the package. As a result, equity markets will likely trend higher, corporate spreads may tighten and the euro expected to gain.

“The currency is a clear beneficiary as it benefits from higher yields and stronger growth prospects,” said Guillermo Felices, global investment strategist at PGIM Fixed Income.

The comments and opinions contained herein are based on and/or derived from publicly available information from sources that PGIM believes to be reliable. We do not guarantee the accuracy of such sources of information and have no obligation to provide updates or changes to these materials. This material is for informational purposes and sets forth our views as of the date of this article. The underlying assumptions and our views are subject to change.

Taggart Davis

VP of Government Affairs

PGIM

Guillermo Felices

Global Investment Strategist

PGIM Fixed Income

How are CIOs responding to the great DB to DC shift as the rest of Europe looks on?

Germany’s decision to relax its borrowing limits signals a seismic shift in its economic strategy, unlocking over €1 trillion in potential spending.

Germany is entering a pivotal moment in its political and economic landscape. Discover the strategic implications for investors after their recent election.