Interpreting the probability of recession

Noah Weisberger, Managing Director, PGIM Institutional Advisory & Solutions, discusses how investors can assess and interpret recession.

12 giu 2023

Recessions are a regularity of the economic landscape. While each recession has its own unique set of characteristics, recessions share common attributes with implications for portfolio construction and asset allocation decisions.

However, we often do not realize we are in a recession until long after it has started. To provide a more up-to-date assessment of recession risk, it is common to turn to models that use current conditions to evaluate the probability of a current or future recession.

For CIOs, evaluating the risk of a recession is not just a curiosity. The probability of being in a recession today – or of a recession occurring soon – may shed light on likely forward market performance and to help better position a multi-asset portfolio.

But interpreting recession probabilities can be difficult. Probability estimates can vary widely across recession indicators, and seemingly similar indicators can generate vastly different probabilities.

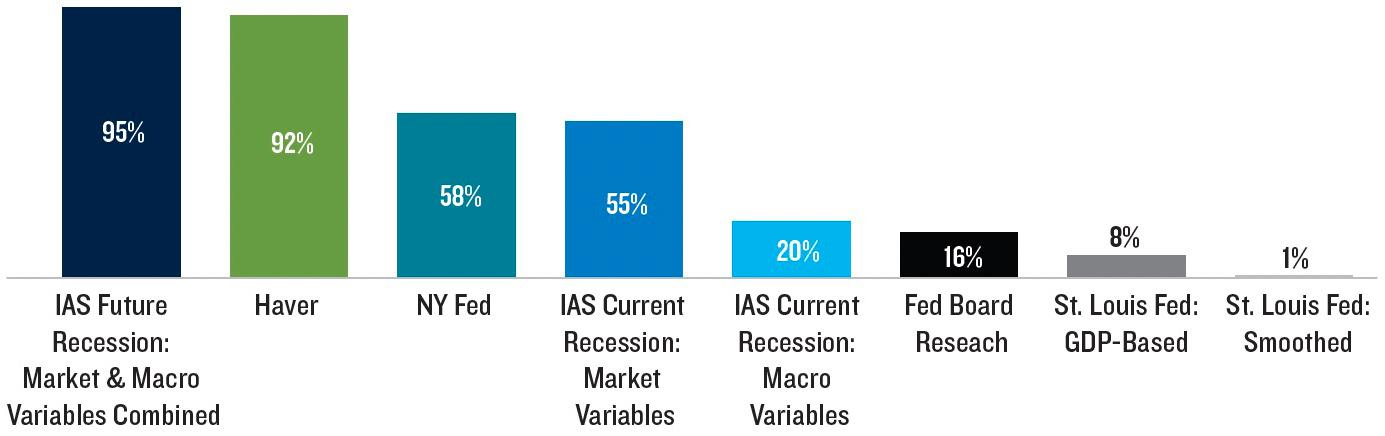

As a case in point, in March 2023, recession probabilities from a variety of recession predictor models ranged from 1% to over 90%. How can a CIO make sense of this? Which signals are more reliable and what, if anything, do these signals foretell about asset class performance?

We explore several issues that CIOs should consider when presented with a recession probability reading:

(as of March 2023)

Note: Model details can be found in the full research paper. NY Fed recession probability estimates are not official forecasts of the Federal Reserve Bank of New York, its president, the Federal Reserve System, or the Federal Open Market Committee. Source: Bureau of Labor Statistics, Federal Reserve Bank of New York, Federal Reserve Bank of St. Louis, Federal Reserve Board, Haver Analytics, NBER, Standard & Poor’s and PMA. For illustrative purposes only.

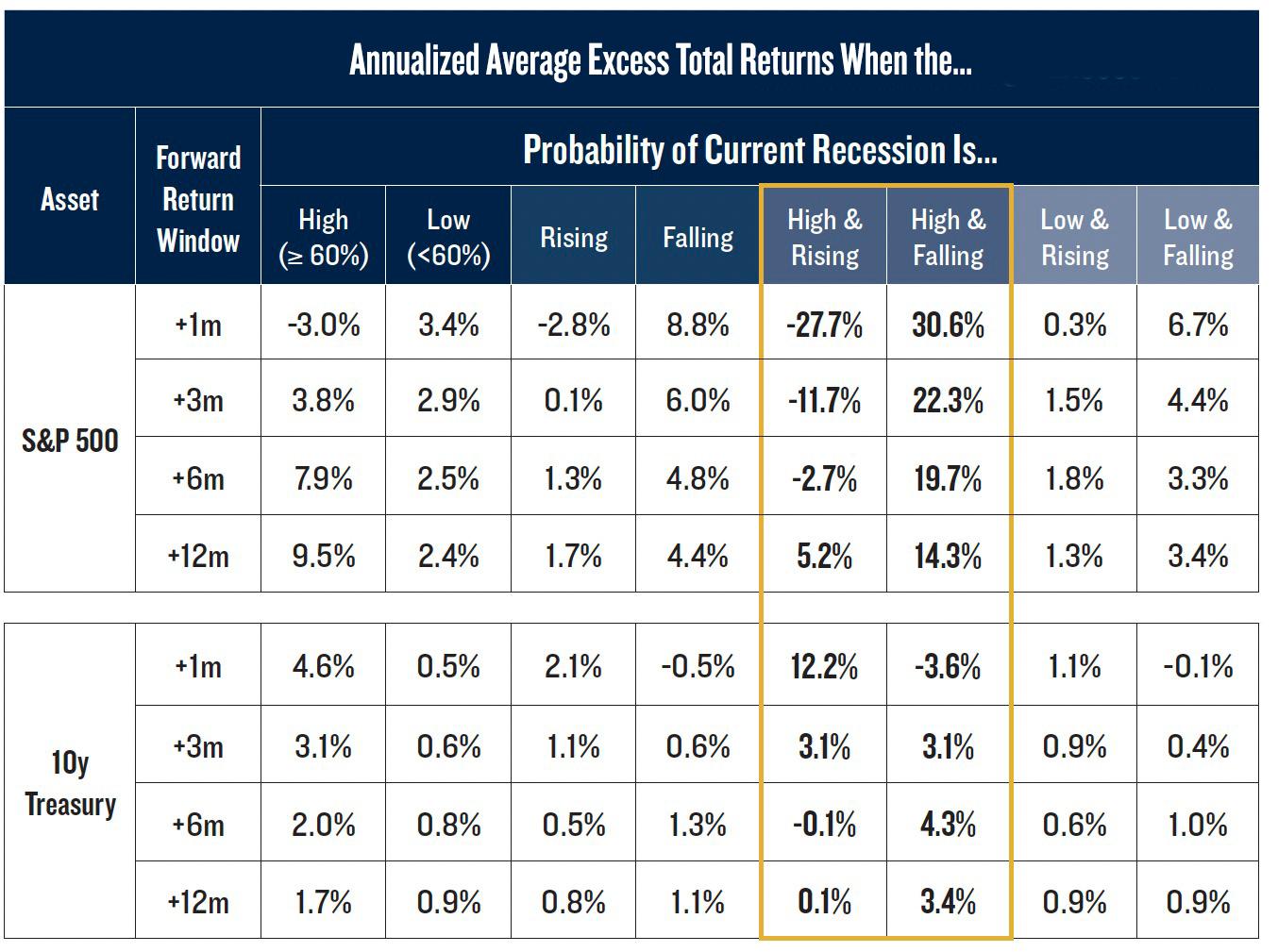

Our research suggests five key takeaways:

Note: Asset class returns are calculated based on a total return price index. Excess returns are relative to 3m LIBOR. Estimated probability of a current (future) recession is based on logit regression; dependent variable equals 1 when the current month (anytime within the next 1-12m) is in recession (NBER defined) and 0 otherwise; regressors are contemporaneous values of SP500, YC, IP and PAY; models are estimated using monthly data from 1954-2019. Source: Bureau of Labor Statistics, Federal Reserve Board, Haver Analytics, NBER, Standard & Poor’s and PMA. For illustrative purposes only.

The Portfolio Research team conducts proprietary research, helping investors navigate asset allocation, portfolio construction, and evolving market landscapes.

Maggiori informazioni

Noah Weisberger, Managing Director, PGIM Institutional Advisory & Solutions, discusses how investors can assess and interpret recession.

We estimate the real-world performance of a private strategy – different vs. the reported performance – and fairly compare it with that of a public strategy.

Liquidity risk can be more severe than volatility risk. Funds may need a designated chief liquidity officer for integrated liquidity management.