Our 12-month outlook explores how the AI investment cycle, evolving rate dynamics, and geopolitical developments are reshaping markets, while highlighting where selectivity, diversification, and income opportunities may be most compelling. Across asset classes and regions, we outline actionable themes to help investors navigate a more complex, higher-yielding environment.

- Tailwinds & Thicker Tails

- New Yield Paradigm

- Diversification Approaches

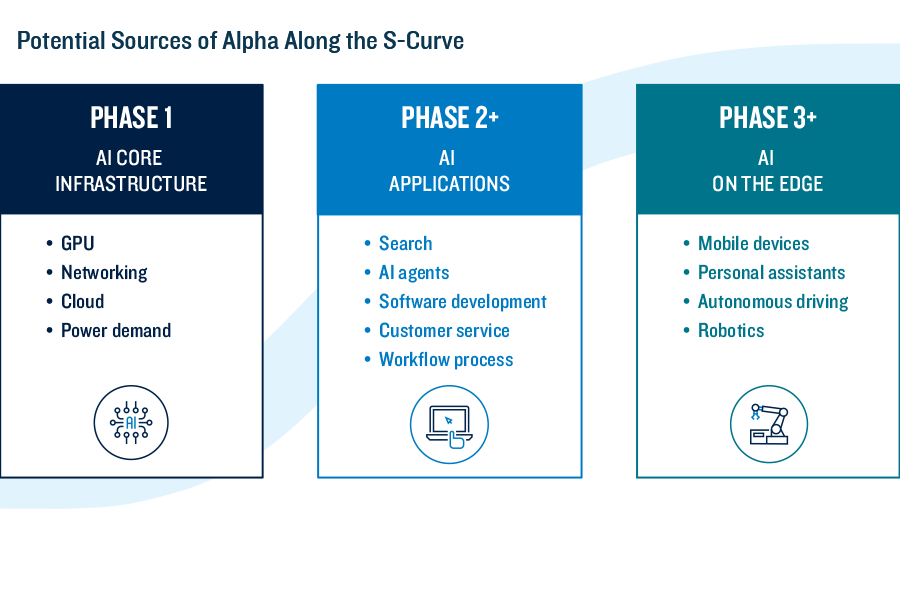

- AI Evolution

Related Strategies

Related Strategies

Related Strategies

5557339