Uncovering Tech-Driven Growth in a Crowded Market

The outperformance of tech-related companies is a reminder that the opportunities are not confined solely to hardware, software, and the internet giants.

How to convert accumulated wealth over one’s working years into a sustainable income stream once in retirement is a complex challenge for most Americans.

To address this difficult financial challenge, defined contribution (DC) plans should broaden their focus from savings accumulation to offering workers the tools and solutions necessary to convert DC plan savings into lifetime retirement income.

It won’t be easy.

In fact, it will require a transformation of the DC industry, one in which DC plans evolve from savings vehicles to true retirement plans that help individuals generate income by managing the risks they face both during their working years and in retirement. The evolution will require outcomes-based retirement programs that deliver reliable, long-term income for retirees. To achieve this, we believe:

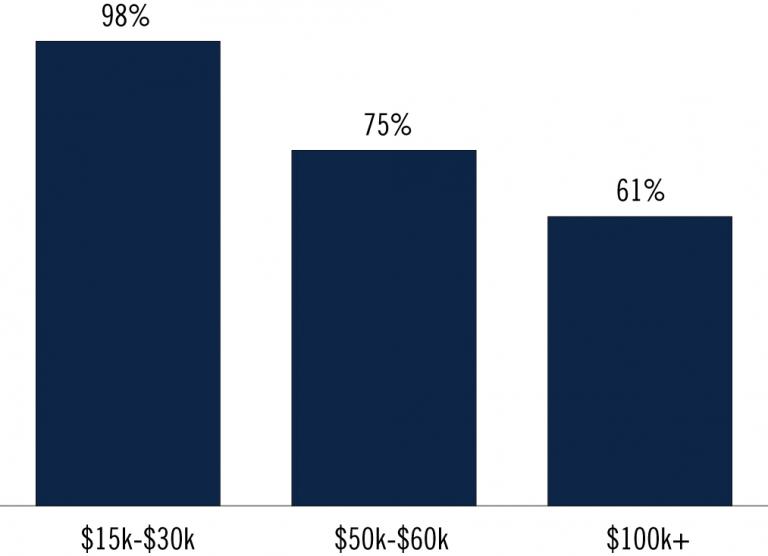

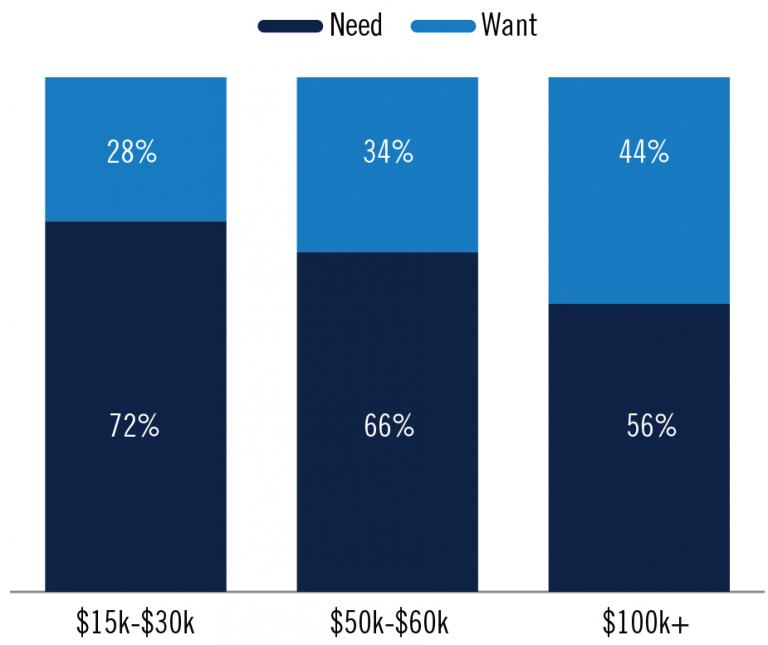

1. An investment methodology is needed that specifically solves for individuals’ unique spend-down goals in retirement. Designing solutions that can effectively provide a stream of income in retirement demands a liability-oriented mindset. Just as institutional investors attempt to meet some form of a liability, participants in a DC plan are tasked with doing the same, although their “liabilities” are the expenses they will face throughout retirement. Applying a one-size-fits-all approach to an income replacement goal can fall short for many reasons, but one main drawback is that it doesn’t address the different spending needs of individuals across the various income cohorts. In addition, by dividing expenses between “Needs” and “Wants” we are able to decompose the income replacement goal and recognize the differing relative importance between the two types of expenses – ultimately leading to a better defined liability. Based on our research, approximately 60% of DC plan participants indicated they need help on spending down their savings during retirement. To meet this need, it is necessary to have both an investment methodology and solutions that are specifically designed to provide the income necessary to meet each retiree’s liabilities.

2. Additional asset classes should be incorporated in the asset allocation strategy to help retirees manage spend-down risks. Most DC plans do not offer access to asset classes that can provide more predictable sources of returns for a time horizon, or duration, on par with the years of drawing down during retirement. Investments such as inflation-linked bonds, high-yield bonds, commodities, real estate (public and/or private), and long-term bonds are not typically available on core menus. We believe the best way for plan sponsors to offer these additional exposures is through multi-asset class solutions that are designed specifically for decumulation. Alternatively, plan sponsors can offer them through a professional investment service, such as a retirement managed account program in which the asset allocation is set by an investment expert. Both paths address the most important issue, which is that participants and retirees require assistance in effectively allocating to extended asset classes and building efficient retirement portfolios.

3. Available guaranteed income sources should be considered as part of the asset allocation process and optimized to help retirees manage the core risk of outliving their savings. We believe a retirement income solution must provide guidance on when participants should consider claiming Social Security based on their unique financial situations. In addition, a solution should have the flexibility to include additional sources of guaranteed income and allocate to these sources based on the varying needs and desires of a participant, availability of products in or outside the DC plan, and the current interest rate/market environment. One option could be to incorporate a guaranteed income solution in a sophisticated fashion as part of the plan default, or qualified default investment alternative (QDIA).

4. An institutional investment approach that leverages the scale and fiduciary oversight offered by DC plans is critical to efficiently building wealth and delivering income. Given changes in capital markets, interest rate cycles, and inflation over time, taking a thoughtful and dynamic approach to investing, while incorporating diversifying, inflation-sensitive, and alternative asset classes that can contribute to more predictable sources of returns in retirement can improve outcomes for retirees. We find that generating 0.35% of net-of-fees alpha, whether through higher gross returns or lower fees, over a lifetime of saving and spending can translate into an additional six years of income in retirement for an individual.

5. Technology is central to delivering personalized advice and solutions by combining our first four retirement income beliefs to address each individual’s particular situation. We believe technology will play a central role in bringing personalized retirement advice and customized solutions to individual retirees within DC plans. The most efficient way to incorporate individuals’ unique liabilities, differing sources of income, and spending needs in a personalized manner is to leverage tomorrow’s best thinking about behavioral finance and technology. Specifically, we believe that advancements in technology, data, and analytics will allow the creation of more personal experiences at scale across channels and buying stages based on the participant’s needs and aspirations.

Combining these tools in a comprehensive retirement income solution can transform DC plans from simply savings plans into retirement plans that are positioned to deliver the lifetime income retirees seek.

Opportunities for long-term investors to thrive

Erfahren Sie mehr

Helping individuals through world’s leading plan sponsors to become retirement ready by meeting their liabilities and managing key risks.

Learn more

The outperformance of tech-related companies is a reminder that the opportunities are not confined solely to hardware, software, and the internet giants.

Unprecedented dislocations in various parts of the Treasury market have resulted in attractive relative value opportunities, including in 10- and 20-year bonds.

Evolving market conditions are supportive of mezzanine debt and other “structured” capital as a relevant source of funding for middle-market upstream companies.

Cities are seeing signs of improved rental growth, benefiting from a sharp increase in hiring intentions that are driving employment and space requirements.

Explore our framework that allows investors to capitalize on alpha opportunities across securities, industries, and countries, while balancing risk.

Private equity secondaries remain one of the top three long-term strategic preferences of investors, ahead of some other well-established strategies.

PGIM does not establish or operate pension plans.