U.S. Part 1- Are We Past the Bulk of U.S. Value Declines?

The decline in U.S. property values has further to run, but due to a combination of investor discipline and more than a little luck, the bottom is in sight.

Investor intentions surveys and investment flows into logistics point to the sector remaining the most favored across Europe. In particular, overseas capital is still chasing logistics stock, over retail and office investments, on the back of a strong structural rental growth outlook for distribution space close to major urban conurbations and transport nodes.

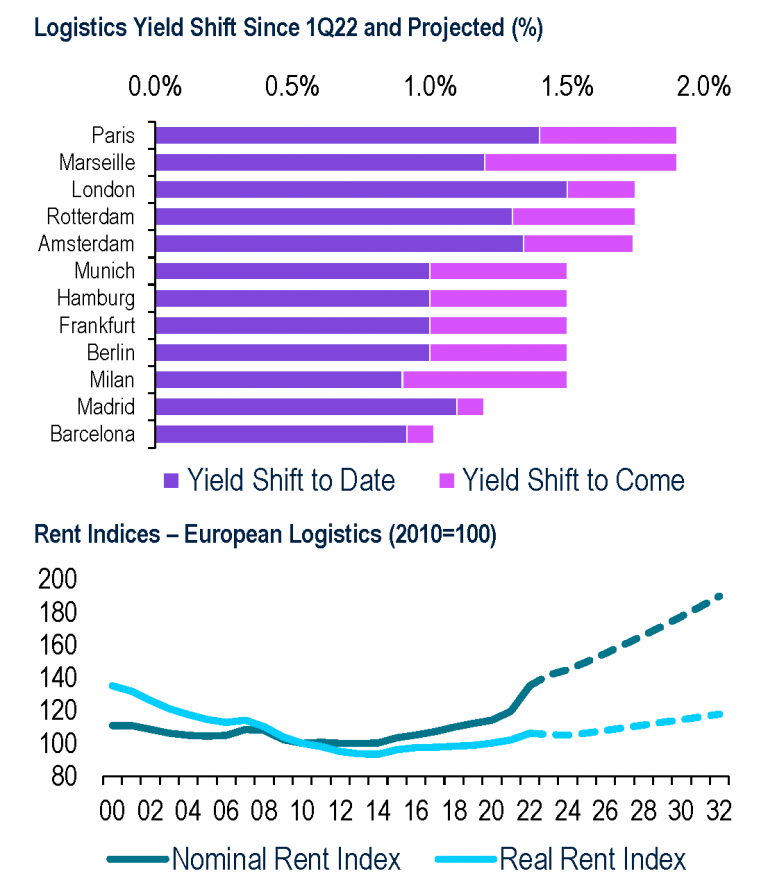

In addition, logistics yields have moved out by more than 100bps in many markets in a short period of time and, based on our estimates, are already two-thirds through the adjustment process that is playing out (Exhibit 3). In cities such as London or Madrid, the yield shift looks nearly done, pricing in resilient rental growth going into the downturn and a positive rental growth outlook looking ahead.

In a broader sense we are seeing a strong structural rental growth story playing out across all of Europe as rents are rising in nominal and real terms on the back of elevated e-commerce adoption rates and supply chain restructuring that is enabling landlords to push inflation through to logistics occupiers (Exhibit 3). This has transformed logistics from a declining real rental sector into one that can absorb elevated inflation and looks to record further real rental growth on the back of structural tailwinds.

However, while it looks like a strong outlook, we have to ask ourselves what could go wrong. Among key risks, European economies have yet to feel the full impact of higher interest rates and there is also rising supply that is hitting the market just when question marks around occupier market performance are emerging. Another trend we are seeing play out is that rental growth is becoming more selective, focused on the best assets in the best markets, which is set to be reinforced by rising ESG regulation driving market bifurcation and limiting investment opportunities (Exhibit 3).

Compared to the other sectors, however, logistics remains in favor among investors who want to allocate capital to real estate as the rental growth outlook remains positive. Even so, the presence of these risks means that we should remain cautious and selective toward acquisitions in the sector, considering only assets that have significantly

The decline in U.S. property values has further to run, but due to a combination of investor discipline and more than a little luck, the bottom is in sight.

The transaction volume of standing assets was US$42 billion in the first half of this year, down almost 50% year-on-year.